The Three Biggest Steps Toward Saving for a Down Payment

The down payment on a mortgage can be one of the biggest hurdles in the journey to homeownership.

It is important to have funds available for a sizable down payment (20% or higher), as this will allow you to forego paying monthly private mortgage insurance. Overall, the equation is quite clear: the higher the down payment, the lower your loan and monthly payment on your mortgage will be.

But how do people show up to the table with, in many cases, tens of thousands of dollars to offer up on their mortgage loan?

Here are three steps to save up for your down payment that are accessible for nearly all buyers with a stable income.

1) First and foremost, determine your down payment goal. Saving is much easier with a tangible goal in mind, rather than stockpiling cash just for the sake of it.

For example, if you and your partner hope to save up enough money for a down payment on a $400,000 home, you should sketch out a timeline and monthly contribution to meet a down payment sum of around $80,000.

Sounds scary, right? But having a figure in mind will make it easier over time to save for your down payment, and the satisfaction of watching your saving balance rise will only drive your determination to get that house. You know, one of the colonials on that beautiful street with the old oak trees and weathered brick that you have been eyeing.

2) Set up a saving account with a high Annual Percentage Yield (APY), and configure an automatic monthly transfer of funds into this account. Designate this money solely to your down payment savings goal.

Another option is a Certificate of Deposit account. These accounts have a minimum term limit for withdrawal. Meaning, you will be charged fees if you are to attempt to take money out of the account before the time limit is up. This could be beneficial if you find saving difficult and also want a higher APY on your down payment savings account.

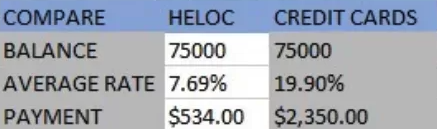

3) Get rid of your credit card debt. Attacking credit card debt and freeing yourself of paying interest on credit card bills will make you primed and ready to start saving for a home.

We know it isn’t easy. Saving for a long term goal can feel tedious at best and demoralizing at worst. 20% on a home loan is a lot of money, but saving over time is a solid possibility when you have the right amount of determination, and most importantly, a plan.

Set a goal, set and account, eliminate credit card debt, and you’ll be on your way in no time.

{kind=link}